Using this analysis from an IMF, World Economic Outlook study; direct ties with Bolivia situation are commented in these type of [brackets] along the whole document:

WORLD ECONOMIC OUTLOOK ANALYSIS

Commodity Exporters Facing the Difficult Aftermath of the Boom

IMF Survey

September 28, 2015

- Commodity-exporting economies likely to slow further given weak commodity price outlook [Bolivia is not “shielded” as the governmental lies led us to believe…]

- Slowdown reflects in part lower growth in potential output [this why the government is relentlessly pushing for the illegitimate re-re-re-election of the coca grower caudillo, before things turn bad… as they control all State powers, like in Venezuela, it will be easier for them to stage a “democratic election” and remain in power]

- Structural reforms to boost growth potential, exchange rate flexibility policy priorities [unthinkable to implement under the egocentric masista “model”]

With a weak outlook for commodity prices, particularly for energy and metals, growth in commodity-exporting emerging and developing economies could slow further over the next few years, says a new study. [no wonder the Bolivian ochlocracy has closed the Mutun Siderurgy… until?]

The study, published in the forthcoming 2015 World Economic Outlook, suggests that the recent declines in commodity prices could shave off one percentage point annually from the growth rate of commodity exporters over 2015-17 as compared with 2012-14. In exporters of energy commodities, the drag is estimated to be even larger—about 2¼ percentage points on average. [which is unfortunately the Bolivian situation; aside of the failure to capture new investments, no new relevant exploration, findings were done in the decade lost under the masismo]

This slowdown is not just a cyclical phenomenon, the study finds. “It has a structural component as well,” says lead author Oya Celasun, Deputy Division Chief in the Research Department. “Investment, and accordingly, potential output, tend to grow more slowly in exporters during commodity price downswings.” [the old rhetoric anti capitalism and delusional poses of grandeur have not only scared away relevant, solid investors, but continue to misled the majority of the Bolivian population who remains ignorant on this gov’s real performance]

The decline in potential growth exacerbates the post boom slowdown, Celasun says. “This means that policymakers in commodity-exporting countries must go beyond demand-side measures and tackle structural reforms to improve human capital, increase investment and, ultimately, unleash higher productivity growth.” [unthinkable under this populist, demagogue government, which has managed to get rid off the institutionality on all areas of government. The desires of the egocentric ruler has also served to a unique purpose, to remain in power, nothing else]

Upswings and downswings

Commodity prices are unpredictable and can be very volatile. They can remain high or low for prolonged periods, giving the impression that their levels are permanent, only to exhibit very sudden and large changes.

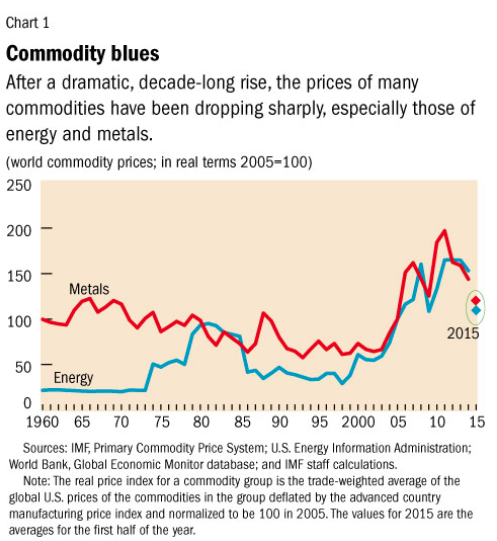

Recent history is no exception. The first decade of the 2000s saw a persistent surge in commodity prices from record lows in the mid-1990s to record highs by 2011. More recently, however, the prices of commodities have fallen again, some in a dramatic fashion, and are expected to remain weak for some time (Chart 1). [a decade has passed under this ruler, and not only over 700 Bolivians had to flee the country, due to political persecution; a number of media companies have fallen under the gov’s pressure, bought or pressured with propaganda money, there is limited freedom of the press, which also resulted in the waste of over $150 billion dollars over this time of bonanza…]

Procyclicality, a common concern

In commodity-exporting economies, output growth, and economic developments more broadly, are unavoidably driven by commodity price cycles. To understand the channels better, the study examines data for more than 40 commodity exporters in emerging and developing economies for the last 50 years. It finds that output and, particularly, investment grow faster during commodity price upswings than in subsequent downswings (Chart 2). Much of this cycle reflects a strong investment response in the commodity-producing sector itself, which spills over into supporting industries such as construction, transportation, and logistics.

But it also reflects other mechanisms. In countries that rely heavily on resource revenues, fiscal policy is often procyclical with respect to the terms of trade. Government spending tends to increase when commodity terms of trade are improving, influencing economic activity more broadly. At the same time, governments, firms, and households in commodity-exporting economies all tend to borrow more easily during commodity booms than during downturns, amplifying the economic cycle set in motion by commodity prices. [Bolivia wasted those resources; in addition: smuggling and narcotrafficking activities have bloomed! which have distorted public perception regarding the real economic situation of our society under the masismo]

Cyclical trends versus structural shifts

The appropriate policy responses depend not only on the extent of the growth slowdown but also whether commodity-price-related fluctuations in output are mostly structural or cyclical in nature. That is, policies would have to be designed differently if commodity price changes affect potential output and not just the cyclical fluctuations around it. [instead, this Bolivian government only thinks on the illegitimate perpetuation in power of the coca grower caudillo, nothing else!]

The study finds that both cyclical and structural factors tend to be at play during commodity-price driven fluctuations in output growth. On average, about two-thirds of the decline in output growth in commodity exporters during a commodity price downswing is cyclical, and one-third is structural, reflecting lower potential growth. This means that for commodity exporters that have enjoyed a prolonged surge in commodity prices, the recent slowdown also reflects weaker growth potential, as investment growth collapses. [and this to make things even worse for Bolivia!]

What to expect going forward

What does the behavior of economic activity during past commodity price cycles imply for the current downswing? While the size and duration of the 2000s commodity boom exceeded its historical average, its reversal could lead to a sharper slowdown now. However, a typical commodity exporter is now better equipped to deal with a downswing than in earlier episodes. [not Bolivia, for sure]

Despite the more pronounced commodity price boom, growth rates over the last decade have been in line with earlier boom episodes and inflation rates have remained more subdued. This suggests that macroeconomic policies were more successful in smoothing the impact of the commodity windfall than in the past, as there was less of a growth boost than one would have expected given the size of the increase. [current Bolivian government use macroeconomic figures to misled the population, while microeconomic reality has pushed the people to a more precarious economic mirage… take for example the price of a kilo of meat, before this government was Bs14 now is over Bs40; or the price of bread, used to be 20 cents and now is over 50 cents…]

More specifically, fiscal policy has been less pro-cyclical—allowing for greater savings out of resource revenues—exchange rates have been more flexible, and financial depth has increased relative to the earlier episodes. All these factors were associated with smaller drops in output growth during previous downswings. [this government have not saved nor invested wisely, boondoggles and white elephant infrastructure to build the myth of the personality of their leader was all that had taken place!]

In addition, commodity exporters are entering the current downswing with stronger external positions, which can also help mitigate the effect of the commodity price downturn on their economies.

What are policymakers to do [none of the conclusions below apply to current Bolivian gov’s priorities/vision. My comments along the whole document, reflect the true nature of the worst government possible in Bolivia, we lost the best economic time ever in our history to the worst ochlocracy possible!]

The findings of the study imply that the growth slowdown in the immediate aftermath of a commodity price boom most likely represents a return to a more sustainable level of output. At the same time, slowing investment and economic capacity can lead to lower potential output growth.

Policymakers in commodity exporting countries therefore need to be careful not to overestimate the extent of excess capacity in their economies. A significant deceleration in growth rates is unavoidable for many economies.

Looking beyond the current juncture, the findings suggest that more flexible exchange rates and policy frameworks that avoid excessive pro-cyclical fiscal spending can help policymakers smooth the impact of commodity price swings on their economies.

Where growth is disappointing, policy efforts that focus on structural reforms to foster sustained medium-term growth are likely to be very fruitful. The structural reform priorities vary across countries, but removing infrastructure bottlenecks, improving the business climate, and enhancing the quality of education are common goals across many.

The authors of this study are Oya Celasun (team lead), Aqib Aslam, Samya Beidas-Strom, Rudolfs Bems, Sinem Kılıc Celik, and Zsoka Koczan, with support from Hao Jiang and Yun Liu and contributions from the IMF Research Department’s Economic Modeling Division and Bertrand Gruss.

http://www.imf.org/external/pubs/ft/survey/so/2015/res092815a.htm