Fitch reports, for Spanish use Pagina Siete’s last bottom link:

Fitch Revises Bolivia’s Outlook to Negative; Affirms IDR at ‘BB-‘

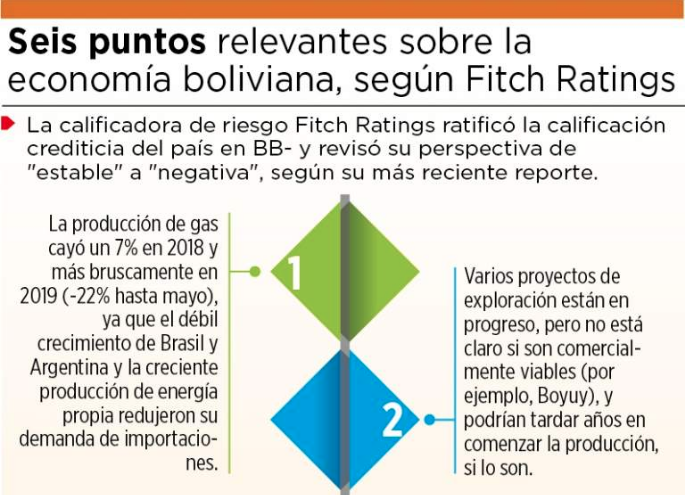

Fitch Ratings – New York – 20 June 2019: Fitch Ratings has affirmed Bolivia’s Long-Term Foreign Currency Issuer Default Rating (IDR) at ‘BB-‘ and revised its Outlook to Negative from Stable.

Fitch Ratings – New York – 20 June 2019: Fitch Ratings has affirmed Bolivia’s Long-Term Foreign Currency Issuer Default Rating (IDR) at ‘BB-‘ and revised its Outlook to Negative from Stable.

KEY RATING DRIVERS

The revision of Bolivia’s Outlook to Negative reflects rising macroeconomic vulnerability posed by the rapid erosion of external and fiscal buffers, being driven in part by adverse developments and future uncertainties in the gas sector – a key source of FX and fiscal revenues. High twin deficits have not fallen as Fitch previously projected despite improved terms of trade, due to a shock to gas export volumes that may not be transitory in nature, and policies fuelling firm domestic demand. Fitch believes these developments have made stabilization of eroding financial buffers more difficult and dependent upon policy adjustments after October 2019 elections. While Fitch expects adjustments will be forthcoming in any election outcome, their magnitude, pace and composition are difficult to predict given a lack of detailed plans among candidates, posing uncertainty around the post-election macroeconomic outlook.

The ratings are supported by an external liquidity position projected to remain relatively strong despite on-going erosion, and the sovereign’s favorable debt profile and cash buffers that reduce financing risks. These strengths are balanced by low per capita income and governance scores, high commodity dependence, and a weak private investment climate rendering growth reliant on expansive policies.

Bolivia’s gas sector is being challenged by a demand shock and supply-side issues. Gas production fell 7% in 2018 and has done so even more sharply in 2019 so far (-22% through May), as Brazil and Argentina’s weak growth and growing own energy production have reduced their import demand. Bolivia recently agreed to a two-year addendum to its contract with Argentina that could pose revenue risks, as it sets lower gas shipments throughout the year and a new price linked to LNG in the winter that may not be higher enough to compensate, although the authorities estimate it will generate an annual revenue gain of up to USD500 million. Supply-side issues pose further uncertainty in the gas sector outlook after a decade of lacklustre investment. Several exploration projects are in progress in 2019, but it is unclear if some key ones are commercially viable (eg. Boyuy), and could take years to begin production if they are.

Falling gas export volumes offset the boost from better prices in 2018, keeping the current account deficit high at 4.9% of GDP, and Fitch projects it will reach 6.0% in 2019 due to the fall in gas revenues so far this year. Large and negative “errors and omissions” in the balance of payments (eg. USD1 billion in 2018) suggest even greater external pressures, which may reflect measurement issues, unregistered contraband or capital flight. These pressures reduced international reserves to USD8.3 billion as of May from USD8.9 billion at end-2018 and USD15.1 billion at end-2014, and the decline has been even greater net of several boosts as the central bank (BCB) has “bolivianized” (ie. converted into local currency) other FX funds corresponding to banks and the sovereign for around USD2 billion since 2014.

Reserves remain high in 2019 in terms of coverage of current external payments (six months) and liquid external liabilities (supporting a 600% liquidity ratio), offering ample scope to manage external shocks. However, they have fallen below the ‘BB’ medians to 20% of GDP and 29% of broad money as of May, signalling potential vulnerability to any home-grown shocks or capital flight. This highlights a difficult policy dilemma surrounding the stabilized XR regime: a devaluation could narrow the current account deficit, but also fuel FX demand in the capital account should it unsettle well-internalised expectations around a stable currency.

The general government deficit rose to 6.0% of GDP in 2018 from 5.0% in 2017 (8.1% from 7.8% at the public sector level), as higher gas prices were not enough to offset lower production volumes, weak non-gas revenues, and resumption of a yearend salary bonus. Fitch expects the general government deficit to rise to 6.4% of GDP in 2019, and 8.5% at the public sector level.

Fiscal deficits lifted general government debt to 39.5% of GDP in 2018 (in line with the historic ‘BB’ median) from 31.2% in 2013, but have been financed to an even greater degree by drawdown of deposits to 11.8% of GDP from 23.2%. Fitch expects financing to rely more heavily on borrowing starting in 2019 (namely via a Eurobond issuance), lifting debt to 44% of GDP by 2020. Fitch estimates a 4%-of-GDP fiscal adjustment over the medium term would stabilise debt/GDP. This could be facilitated by a flexible spending profile dominated by public investment (13% of GDP in 2018), but large cuts would pose trade-offs with growth objectives.

Bolivia’s strong debt profile remains a key credit strength. Near-term maturities are very low, averaging just 1.5% of GDP in 2019 and 2020, and amply covered by cash deposits. Most of the debt stock is owed to multi- or bilateral creditors and the central bank and on concessional terms – reflected in a low interest/revenue ratio of 4.3%, well below the historic 9.3% ‘BB’ median. External bonds total a modest USD2 billion (5.0% of GDP).

Expansive policies guided by an ambitious state-led investment plan (PDES) supported firm real GDP growth of 4.2% in 2018. Fitch projects growth of 3.8% in 2019, but believes the post-2019 outlook is uncertain. The government expects industrialisation projects to lift growth and yield revenues that lower the twin deficits, avoiding a need for a major policy adjustment, but this has not yet occurred as previously projected in the PDES amid delays and profitability issues. In the absence of a greater windfall from these projects or external tailwinds, pressure for policy adjustments could build. Fitch projects policy tightening to slow growth to 3% in 2020 and beyond, but this is hard to predict given uncertainty around the post-election policy strategy, and risks of a greater slowdown cannot be ruled out.

Monetary policy has been further loosened to support credit objectives as liquidity has sagged. Credit growth of 10.4% yoy as of May is far above deposit growth of 3.7%. Fitch expects credit growth to ease now that banks have mostly achieved credit allocation quotas set in a 2013 law, and given lower bank capital and liquidity ratios, though adequate, offer less scope for lending without commensurate deposit funding. Inflation at 1.7% as of May remains low despite monetary stimulus and direct BCB lending to SOEs and the Treasury, given the demand this has supported has largely gone to imported goods and accommodated via reserve drawdown.

President Evo Morales will run for a fourth term in upcoming elections in October, following the overturning of constitutional term limits by the courts last year. Polls suggest the election could be competitive, with Morales leading polls but with a large number of undecided voters. Fitch expects macroeconomic policy adjustments to contain economic risks would be forthcoming in any election scenario, although the result could condition the adjustment strategy and timing, while microeconomic policies could vary significantly.

KEY ASSUMPTIONS

Fitch expects Brent oil prices to average USD65/b in 2019 and USD62.5/b in 2020, affecting Bolivian gas prices (linked to global oil benchmarks with a three to six month lag).

RATING SENSITIVITIES

The main factors that could individually, or collectively, lead to a downgrade include:

–Persistence of high twin deficits that erode external and fiscal liquidity buffers; for example, due to lack of policy adjustments and/or a lasting decline in gas exports;

–A pronounced slowdown leading to macroeconomic or financial instability;

–Evidence of external financing constraints.

The Rating Outlook is Negative. Consequently, Fitch does not currently anticipate developments with a high likelihood of leading to a positive rating change. However, the main factors that could lead Fitch to Stabilize the Outlook include:

–A reduction in the current account deficit that helps stabilise FX liquidity metrics; for example, driven by policy adjustments or higher export revenues;

–Sustained fiscal deficit reduction that improves public debt dynamics and preserves fiscal liquidity buffers;

–Evidence of improvement in governance and the business climate that supports stronger investment and growth prospects.

| VIEW ADDITIONAL RATING DETAILS |

Additional information is available on http://www.fitchratings.com

APPLICABLE CRITERIA

DISCLAIMER

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK: HTTPS://WWW.FITCHRATINGS.COM/UNDERSTANDINGCREDITRATINGS. IN ADDITION, RATING DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE AGENCY’S PUBLIC WEB SITE AT WWW.FITCHRATINGS.COM. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. FITCH’S CODE OF CONDUCT,

COPYRIGHT

Copyright © 2019 by Fitch Ratings, Inc., Fitch Ratings Ltd. and its subsidiaries. 33 Whitehall Street, NY, NY 10004. Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved. In issuing and maintaining its ratings and in making other reports (including forecast information), Fitch relies on factual information it receives from issuers and underwriters and from other sources Fitch believes to be credible. Fitch conducts a reasonable investigation of the factual information relied

SOLICITATION STATUS

The ratings above were solicited and assigned or maintained at the request of the rated entity/issuer or a related third party. Any exceptions follow below.

ENDORSEMENT POLICYFitch’s approach to ratings endorsement so that ratings produced outside the EU may be used by regulated entities within the EU for regulatory purposes, pursuant to the terms of the EU Regulation with respect to credit rating agencies, can be found on the EU Regulatory Disclosures page. The endorsement status of all International ratings is provided within the entity summary page for each rated entity and in the transaction detail pages for all structured finance transactions on the Fitch website. These disclosures are updated on a daily basis.

https://www.fitchratings.com/site/pr/10079978

For Spanish, use this link