By Germán Huanca Luna, Urgente.bo:

While the government labels the Plurinational Assembly’s refusal to approve international loans as “economic sabotage,” from an economic standpoint, what is unfolding is a disaster that has been forewarned for years. The current situation is the result of an economic policy that has prioritized public spending beyond the country’s real production capacity. In this sense, the government must take full responsibility for the catastrophe it has led Bolivians into by implementing an unsustainable economic strategy.

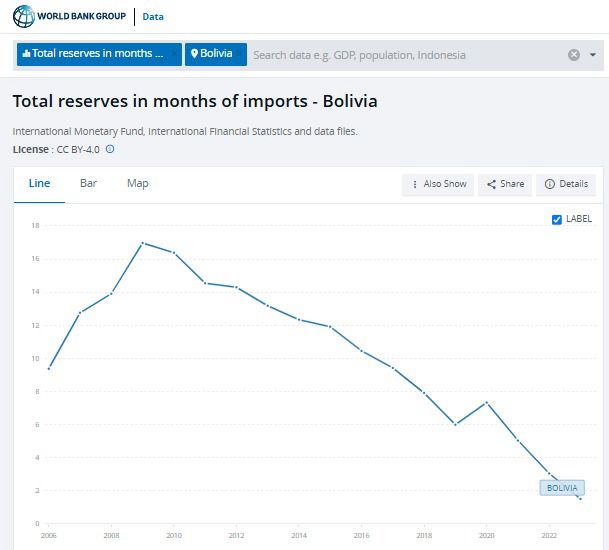

Regarding macroeconomic figures, various analysts have scrutinized them. However, today we want to focus on one indicator that reflects trade policy behavior and the availability of dollars in the country: the ratio between International Reserves and Imports, which gives us the Total Reserves in months of imports.

According to data from the World Bank (https://data.worldbank.org/), in 2006, when the MAS-IPSP took power, Bolivia could cover up to nine months of imports with its international reserves. With gas revenues in the following years, this ratio peaked in 2009, allowing the country to cover up to 17 months of imports before declining to six months by 2019. During the Áñez administration, efforts were made to recover six to seven months of import coverage by the end of 2020. However, from that year onward, this ratio began to plummet alarmingly, reaching 2023, when reserves could only cover a month and a half of imports. Currently, there is no updated data on this indicator, and it is assumed that reserves are insufficient to cover even one month.

This behavior reflects the irrationality of the economic policy implemented by Evo Morales, along with then-Minister of Economy Luis Arce, which has continued under Arce Catacora’s government. The creation of state-owned enterprises, infrastructure projects without economic justification, and unnecessary public spending increases have been key decisions leading to this crisis. As export revenues declined, the government chose to increase external debt, leaving the country bankrupt and deeply indebted.

It is important to note that neither business owners, currency exchangers, nor importers are responsible for this crisis. The current shortage of gasoline and diesel is the sole responsibility of the Bolivian government. In particular, the Central Bank of Bolivia, the Executive Branch, and the Plurinational Assembly bear responsibility for allowing the use of International Reserves below minimum thresholds, severely impacting dollar liquidity in the economy.

The government must urgently take responsibility for the crisis and stop delaying its resolution. The country needs drastic measures to overcome this situation: a sharp reduction in public spending and the removal of export restrictions to generate a trade and fiscal surplus, restoring confidence in the economy and improving dollar inflows. If this is not possible, Bolivia will have to resort to an international loan from the IMF or the World Bank specifically to balance the payments deficit and inject liquid dollars into the Bolivian economy.

What is really behind the government’s request for international loans is not a structural solution but merely a short-term fix to get through the elections. The government wants dollars to hand over to YPFB to pay for gasoline and other international commitments. But this will not address the underlying problems. Even if currency swaps are carried out, Bolivia will remain trapped in the same vicious cycle of dependency on loans and external debt.

It is time for the MAS-IPSP and Arce’s government to take full responsibility for the economic crisis. You created this crisis, and the public needs to know it. The real economic sabotage comes from the government, the result of poor economic management. The challenge is clear: addressing the international reserves crisis is crucial to ensuring economic stability and preventing the fuel shortage from continuing to paralyze the country.

*Master in Financial Economics

Por Germán Huanca Luna, Urgente.bo:

Mientras el gobierno califica de “sabotaje económico” a la negativa de la Asamblea Plurinacional para la aprobación de los créditos internacionales, desde el ámbito económico lo que se vive es un desastre que hemos venido anunciando desde hace varios años. La situación actual es el resultado de una política económica que ha priorizado el gasto público por encima de las posibilidades reales de producción del país. En este sentido, el gobierno debe asumir la responsabilidad completa por el desastre al que ha conducido a los bolivianos, debido a la aplicación de una estrategia económica insostenible.

En cuanto a las cifras macroeconómicas, todas han sido objeto de análisis por parte de diferentes analistas. Sin embargo, hoy queremos centrarnos en un indicador que refleja el comportamiento de la política comercial y la tenencia de dólares en el país: la relación entre las Reservas Internacionales e Importaciones, que nos da el indicador Total Reservas en meses de importaciones.

Según los datos del Banco Mundial (https://data.worldbank.org/), en el año 2006, cuando el MAS-IPSP asumió el gobierno, Bolivia podía cubrir hasta 9 meses de importaciones con sus reservas internacionales. Con los ingresos provenientes del gas en los años siguientes, la relación alcanzó un pico en 2009, donde el país podía cubrir hasta 17 meses de importaciones, luego cayó hasta 6 meses el año 2019. Durante el gobierno de Añez, se hizo un esfuerzo de recuperar 6 a 7 meses de importaciones hasta finales del 2020. Sin embargo, a partir de ese año, esta relación comenzó a descender de manera alarmante, hasta llegar a 2023, cuando las reservas solo alcanzan para cubrir 1 mes y medio de importaciones. Actualmente, no contamos con información actualizada sobre este indicador y damos por supuesto que no alcanza ni para un mes.

Este comportamiento refleja la irracionalidad de la política económica implementada por Evo Morales, junto con el entonces ministro de Economía, Luis Arce, y que ha continuado bajo el gobierno de Arce Catacora. La creación de empresas estatales, proyectos de infraestructura sin justificación económica y el aumento del gasto público innecesario han sido algunas de las decisiones clave que llevaron a esta crisis. A medida que los ingresos por exportaciones disminuían, el gobierno optó por incrementar la deuda externa, lo que ha dejado al país arruinado y profundamente endeudado.

Cabe señalar que ni los empresarios, ni los librecambistas, ni los importadores son responsables de esta crisis. La actual escasez de gasolina y diésel es responsabilidad exclusiva del gobierno de Bolivia, particularmente del Banco Central de Bolivia, el Poder Ejecutivo y la Asamblea Plurinacional tienen responsabilidad, por haber autorizado el uso de las Reservas Internacionales por debajo de los límites mínimos, afectando gravemente la liquidez de dólares en la economía.

Es urgente que el gobierno se haga responsable de la crisis y deje de dilatar la solución del problema. El país necesita medidas drásticas para superar esta crisis: recortar el gasto público de manera abrupta y eliminar las trabas a las exportaciones, con el fin de generar superávit comercial y fiscal que permita recuperar la confianza en la economía y mejorar la captación de dólares. En caso de no ser posible, Bolivia deberá recurrir a un crédito internacional del FMI o del Banco Mundial, específicamente para equilibrar la balanza de pagos e inyectar dólares líquidos en la economía boliviana.

Lo que realmente está detrás de la solicitud de créditos internacionales por parte del gobierno no es una solución estructural, sino simplemente un paliativo coyuntural hasta llegar a las elecciones. El gobierno quiere dólares para entregárselos a YPFB y pagar por la gasolina y otros compromisos internacionales. Pero esto no resolverá los problemas de fondo. Incluso si se realizan swaps de monedas, seguiremos en el mismo círculo vicioso de dependencia de préstamos y deuda externa.

Es hora de que el MAS-IPSP y el gobierno de Arce asuman la responsabilidad plena de la crisis económica. La crisis la crearon ustedes, y la población necesita saberlo. El verdadero sabotaje económico proviene del gobierno, producto de una mala administración económica. El desafío está claro: abordar la crisis de las reservas internacionales es crucial para garantizar la estabilidad económica y evitar que la escasez de combustible siga paralizando al país.

*Master en Economía Financiera

https://www.urgente.bo/noticia/desastre-económico-en-fase-terminal